GST Registered Company: A Comprehensive Guide to Navigate Singapore’s Tax for Business Growth

- Tan Wei Jie

- Aug 2, 2025

- 26 min read

Overview of Business Environment in Singapore

Singapore stands as the crown jewel of Southeast Asia's business landscape, offering an unparalleled combination of strategic advantages that have made it the preferred destination for entrepreneurs, multinational corporations, and forward-thinking business professionals.

Whether you're a local visionary or an international investor looking to start a business in Singapore, the city-state offers an environment ripe for growth. Strategically positioned between the East and West, Singapore's political stability and pro-business climate have made it one of the best places to start a business.

The local business environment is mature and is well-positioned to serve businesses of all sizes. From a plethora of banking networks, logistics, and a global talent pool, Singapore attracts the finest companies to set up office here. Over the years, the influx of business from diverse industries has allowed both local and multinational corporate service providers to thrive. As key players in the business ecosystem, corporate service providers facilitate business, offering essential services and advice on multiple issues of the business environment.

Tax in Singapore - GST

Tax policies in Singapore have always been pro-business. Stable policies and a good business ecosystem are critical in attracting foreign companies. However, compliance obligations remain, and we will discuss them further in the latter part of this article about GST Registered Companies.

A key aspect of this environment, and one that often sparks questions, is the Goods and Services Tax (GST). In foreign countries, it may also be known as Value-added Tax (VAT). Understanding GST is not just about compliance; it's about optimizing your business's financial health and leveraging tax benefits. This comprehensive guide will delve deep into the intricacies of GST for companies registered in Singapore, with a focus on helping you navigate its complexities, avoid common pitfalls, and ultimately, contribute to your business's success.

Understanding GST (Goods and Services Tax) in Singapore

The Goods and Services Tax (GST) in Singapore, often referred to as a broad-based consumption tax, is levied on the import of goods into Singapore, as well as on nearly all supplies of goods and services within Singapore. For businesses, comprehending the essence of GST and its implications is paramount. It’s a tax that directly impacts your pricing strategies, cash flow, and accounting practices.

Essence of GST and the Types of Supply

At its core, GST functions as a value-added tax. Businesses that are GST registered in Singapore collect GST on behalf of the government from their customers (output tax) and can claim back the GST they’ve paid on their business purchases and expenses (input tax). The difference between output tax and input tax is what’s remitted to or refunded by the Inland Revenue Authority of Singapore (IRAS).

As a broad-based consumption tax, the GST system seeks to tax the end-user of goods and services. Unlike tiered income taxes, the GST system operates on a fairly broad basis, taxing those who consume.

There are several types of supply under Singapore GST:

Standard-rated supplies: These are taxable supplies where GST is charged at the prevailing rate (currently 9%). Most goods and services supplied in Singapore fall under this category.

Zero-rated supplies: GST is charged at 0% for these supplies. This primarily applies to exports of goods and international services. While no GST is collected from the customer, businesses making zero-rated supplies can still claim input tax on their purchases, making them attractive for export-oriented businesses.

Exempt supplies: Certain goods and services are exempt from GST, meaning no GST is charged on them, and businesses making these supplies cannot claim input tax on related purchases. Common examples include financial services and the sale and lease of residential properties.

Out-of-scope supplies: These are not subject to GST in Singapore. Examples include sales of goods outside Singapore that do not involve Singapore, and certain third-country trade.

Understanding these distinctions is crucial for accurate GST calculation and compliance.

Mandatory vs. Voluntary GST Registration Details

One of the most frequently asked questions for businesses, especially those newly incorporated, revolves around GST registration. Is it mandatory, or can a company choose to register for GST in Singapore voluntarily?

Mandatory Registration: A business is legally required to register for GST if its taxable turnover (the total value of all standard-rated and zero-rated supplies) for the past 12 months exceeds S$1 million.

Alternatively, if a business can reasonably expect its taxable turnover in the next 12 months to exceed S$1 million, it must also register. It is crucial for companies to continuously monitor their taxable turnover to ensure timely registration and avoid penalties. This applies to both sole proprietor and limited partnership setups.

Voluntary Registration: Even if a business does not meet the mandatory registration threshold (taxable turnover exceeding S$1 million), it can choose to register for GST voluntarily.

This is a strategic decision that carries both advantages and disadvantages, which we will explore in detail later in this guide. Generally, businesses that incur significant GST on their purchases, such as those with substantial startup costs or import activities, might find voluntary registration beneficial as it allows them to claim input tax.

Impact and Compliance Requirements for GST-Registered Companies

Once a company becomes GST registered in Singapore, a new set of responsibilities and compliance requirements comes into play. The impact extends across various facets of the business:

Pricing: Businesses must factor in GST when setting prices for their goods and services. The price displayed to consumers should generally be GST-inclusive, or clearly state that GST will be added. (You may be surprised that this exception is only given to F&B and Hotel businesses)

Invoicing: GST-registered companies are required to issue tax invoices that comply with IRAS regulations. These invoices must clearly show the GST amount charged, the GST registration number of the supplier, and other prescribed details. A guideline on how a tax invoice should be is available at IRAS’s official website. IRAS had also rolled out the adoption of the GST InvoiceNow requirement progressively for newly incorporated companies that register GST voluntarily.

Record-keeping: Detailed and accurate records of all sales and purchases, including tax invoices, credit notes, and debit notes, must be maintained for a period of at least five years. These records are essential for supporting input tax claims and for audit purposes. While this requirement is not new, as all business documents must be retained for at least 5 years for corporate tax purposes, being GST registered increases the need for proper documentation.

GST Filing: GST-registered businesses are typically required to file GST returns (Form 5) to IRAS on a quarterly basis, usually within one month from the end of their accounting period. This involves reporting total output tax collected and total input tax claimed. For businesses engaged in specific activities like imports, additional declarations might be required. The additional requirement to file GST tax returns (F5 Tax form) is probably the most prominent change a business owner would observe if they transition to a GST Registered company. While the filing is done quarterly, a timely set of accounting records will be required to support the filing. Hence, it is common for business owners to relook into key processes to support GST filing and tax compliance.

Payment/Refund: Based on the filed GST return, businesses either pay the net GST due to IRAS or receive a refund if their input tax exceeds their output tax. Be it payment or receipts, this amount may impact a company’s cash flow, especially if the business’s monthly receipts are high in volume and/or value.

Non-compliance with tax regulations can lead to significant penalties, including fines and imprisonment in severe cases. Therefore, understanding and adhering to these requirements is not optional but a fundamental aspect of operating a GST registered company in Singapore. This is where professional services, like those offered by corporate service providers, can prove invaluable in ensuring meticulous compliance and allowing business owners to focus on their core operations.

This initial section provides a foundational understanding of GST in Singapore, setting the stage for a deeper dive into voluntary registration, import/export considerations, common mistakes, and the critical role of compliance and professional support.

Voluntary GST Registration: Pros and Cons

For many newly incorporated companies in Singapore, the decision to voluntarily register for GST is a significant one. While mandatory registration thresholds are clear, choosing to opt in before reaching that threshold requires careful consideration of the benefits and drawbacks. This strategic choice can significantly impact a company's cash flow, administrative burden, and competitive positioning.

Benefits of Voluntary GST Registration

Voluntary GST registration can offer several compelling advantages, particularly for businesses that fall into specific categories:

Claiming Input Tax: This is arguably the most significant benefit. If your business incurs a substantial amount of GST on its purchases, expenses, or capital expenditures (e.g., purchasing equipment, office renovation, marketing services, professional fees), being GST-registered allows you to claim back this input tax. This can lead to considerable cost savings and improve your cash flow, especially during the initial setup phase of a Singapore business incorporation.

Example: A technology startup invests heavily in IT infrastructure and software, incurring significant GST. Voluntary registration allows them to reclaim this GST, reducing their overall expenditure.

Enhanced Business Credibility and Perception: For some clients and business partners, particularly larger corporations or international entities, working with a GST-registered company can signal a certain level of professionalism, stability, and legitimate business operations. It can be perceived as a mark of a serious and established business, fostering trust and potentially opening doors to larger contracts.

Zero-Rating for Exports and International Services: If your business is involved in exporting goods or providing international services, voluntary GST registration is crucial. These supplies are typically zero-rated, meaning you charge 0% GST to your overseas customers, making your services more competitive globally. More importantly, you can still claim input tax on the expenses incurred to generate these zero-rated supplies. This is a decisive advantage for export-oriented businesses and those involved in global trade.

Leveling the Playing Field: In industries where competitors are already GST-registered, opting for voluntary registration can help you maintain competitive pricing. If you are not registered, you cannot claim input tax, meaning your costs are effectively higher, which might force you to either absorb the cost or charge higher prices, potentially disadvantaging you.

Do note that if your business provides exempt supplies, the input tax incurred in the making of exempt supplies is not claimable unless the De Minimis Rule is satisfied. The De Minimis Rule allows GST-registered businesses to claim input tax on exempt supplies.

Drawbacks of Voluntary GST Registration

While the benefits can be substantial, voluntary GST registration also comes with its share of disadvantages and increased responsibilities:

Increased Administrative: Being a GST registered company significantly increases your administrative workload. You will need to meticulously track all sales and purchases, issue GST-compliant invoices, maintain accurate records, and file Quarterly Accounting GST returns promptly. Businesses often seek a fuss-free solution, such as outsourcing this segment to a corporate service provider.

Impact on Small Businesses: For small businesses or startups with limited resources, this additional administrative burden can be overwhelming and divert focus from core business activities.

Higher Compliance Costs: To manage the increased administrative tasks, businesses may need to invest in accounting software, train staff, or outsource their GST compliance to professional firms.

Impact on Pricing and Competitiveness (for B2C Businesses): If your primary customers are individuals (Business-to-Consumer or B2C), adding GST to your prices can make your products or services more expensive and potentially less attractive compared to non-GST registered competitors. Consumers generally bear the brunt of the GST, and a price increase might deter price-sensitive customers.

Consideration: If your client pool is generally GST-registered customers, this impact is less significant as they can typically claim the GST back as input tax (assuming that they are GST registered).

Cash Flow Implications: While input tax claims can improve cash flow, there might be periods where output tax (GST collected) significantly exceeds input tax (GST paid), requiring you to remit a large sum to IRAS. This can temporarily strain cash flow, especially if collections from customers are slow. Hence, cash flow monitoring may be something you would wish to place more emphasis on as a business owner.

The decision to voluntarily register for GST should align with your business model, target market, expected turnover, and capacity to handle the increased administrative and compliance requirements. A thorough cost-benefit analysis, possibly with the guidance of a professional, is highly recommended.

GST for Imports and Exports

Singapore's status as a global trading hub means many businesses are involved in the import and export of goods. Understanding how GST applies to these activities is crucial for managing costs, optimizing cash flow, and ensuring compliance. The rules for imports and exports are distinct from those for local supplies and offer unique opportunities for GST registered company to manage its tax obligations effectively.

Understanding GST Claims on Imports and Zero-Rated Warehouses

When goods are imported into Singapore, GST is generally payable on the value of the goods, including customs duties and freight/insurance costs. This import GST can be a significant upfront cost for businesses. However, to GST-registered firms, this import GST can often be claimed back as input tax, provided the goods are imported to make taxable supplies.

There are several schemes and facilities designed to alleviate the cash flow impact of import GST for eligible businesses:

Import GST Deferment Scheme (IGDS): Under this scheme, GST-registered businesses can defer the payment of import GST at the point of importation. Instead, the import GST is accounted for in their quarterly GST returns, effectively converting it into a claimable input tax without an upfront cash outlay. This significantly improves cash flow for businesses with high import volumes. Eligibility criteria apply, and companies need to apply to IRAS for approval. One of the key requirements for a company under IGDS is to file GST monthly.

Major Exporter Scheme (MES): The MES is designed for businesses that export a substantial portion of their goods. Under MES, approved businesses can import goods and make purchases of local goods and services without incurring GST upfront. Similar to IGDS, the GST is instead accounted for in their GST returns. This scheme is particularly beneficial for large trading companies or manufacturers with significant export activities, as it dramatically reduces the cash tied up in GST.

Zero-Rated Warehouses (Customs Bonded Warehouses): These are designated areas where imported dutiable goods can be stored without the immediate payment of customs duties and GST. Goods can remain in these warehouses for an extended period, and duties and GST are only payable when the goods are removed from the warehouse for local consumption. If the goods are subsequently re-exported from the zero-rated warehouse, no duties or GST are paid at all. This is highly beneficial for businesses involved in transit trade or those with fluctuating demand, allowing them to defer tax payments until the goods are actually sold or consumed locally.

Types of Zero-Rated Warehouses: These include Licensed Warehouses (LWs) and Zero GST Warehouses (ZGWs). ZGWs specifically cater to non-dutiable goods.

Approved Contract Manufacturer and Trader (ACMT) Scheme: This scheme allows approved contract manufacturers and traders to defer import GST and GST on local purchases of raw materials/goods.

Businesses frequently importing goods should explore these schemes to optimize their cash flow and reduce the administrative burden associated with import GST.

Drop Shipping – Trading & Ecommerce

Drop Shipping has long been a common practice for trading companies. The rise of e-commerce and the development of marine logistics have fueled the growth of drop shipping. (No surprise that Singapore is a trading hub and a logistics hub concurrently) In a typical drop shipping arrangement, the seller (the Singapore company) takes customer orders but does not hold inventory. Instead, the order is fulfilled by a third-party supplier (often located overseas), who ships the goods directly to the customer.

There are generally two models of drop-shipping. The first is a business-to-consumer model where the consumer is usually located within Singapore. This is a common model for bulk purchase or collating of multiple orders and is often seen in the E-commerce scene.

The next drop-shipping model is a business-to-business arrangement. This setup usually involves a Singapore “middleman” who purchases from an overseas supplier and sells it to a local company or, in some cases, sells the goods to an overseas customer. In the latter scenario, the goods would not have entered Singapore’s territory, and such practices are prevalent for trading companies, especially commodities and energy firms.

The GST implications depend on the flow of goods and the parties involved:

If the supplier is overseas and the customer is in Singapore:

Business-to-Consumer (B2C) Drop Shipping: For GST purposes, if the overseas supplier ships directly to the Singapore customer, the import GST is usually borne by the customer upon importation (if the value exceeds the low-value goods relief threshold). The Singapore drop shipper's sale to the customer is considered a local supply and is subject to GST if the drop shipper is GST-registered and the sale value meets the threshold.

Business-to-Business (B2B) Drop Shipping: If the Singapore company is purchasing from an overseas supplier and selling to a Singapore business, the Singapore company is essentially the importer of record and would be liable for import GST (regarded as a taxable sale). If the Singapore company is GST-registered, it can claim this import GST as input tax. The subsequent sale to the Singapore customer would be a standard-rated supply. This model is typically used for collective bulk purchases and is more commonly seen in the sole-distributor model.

If the customer is overseas:

This is a common practice for commodity trading companies. For the trading of physical goods, a Singapore firm may purchase from one country and ship the goods directly to another country where the customer is located. The goods do not physically enter Singapore, and in such an arrangement, this supply is regarded as out-of-scope supplies.

Given the complexities of international trade and e-commerce models, it is highly advisable for businesses engaged in import/export or drop shipping to seek professional advice from a tax consultant or a corporate service provider to ensure full GST compliance and optimize their tax position.

Common GST Mistakes and How to Avoid Them

Even for diligent businesses, navigating the nuances of GST can be challenging, and mistakes can lead to significant penalties, financial losses, and compliance issues. Understanding the most common pitfalls is the first step towards avoiding them and ensuring your GST registered company remains compliant.

Four Common Errors for GST Filing – Things to note

Here are four pervasive GST mistakes businesses often make and practical advice on how to steer clear of them:

Incorrectly Claiming Input Tax

This is perhaps the most frequent and costly error. Companies may claim input tax on expenses that are not eligible, or do so without proper supporting documentation.

The Mistake:

Claiming GST on non-business expenses: This includes personal expenses of owners or employees, or expenses that do not relate directly to the generation of taxable supplies. Although this may seem straightforward, it is challenging in practice, especially for family-owned businesses or entities with poor accounting records. Expense management can also be cumbersome if there are voluminous expenses.

Claiming GST to make Exempt Supplies: There might be further complications if the business is claiming input tax to make partial exempt supplies (Refer to De Minimis Rule)

Absence of valid tax invoices: Input tax cannot be claimed without a proper tax invoice from a GST-registered supplier. Proforma invoices, delivery notes, or mere receipts are generally insufficient. The tax invoice must show the supplier's GST registration number, business name, the amount of GST charged, and other prescribed details such as Unique Entity Number (UEN).

Claiming GST on disallowed expenses: Certain expenses or business transactions are specifically disallowed for input tax claims, such as passenger motor car expenses (including GST incurred on purchasing, renting, or maintaining passenger cars and fuel for them), and medical expenses (unless they are provided to employees under a contract of service as an entitlement or obligation). IRAS’s website offers a clear list (with worked examples) on disallowed expenses. However, it may be difficult in practice, especially when expenses are wrongly classified during the accounting phase or companies do not have the necessary capabilities for tax compliance.

Incorrect apportionment for mixed-use assets: If an asset is used for both business and personal purposes, or both taxable and exempt supplies, the input tax must be apportioned correctly. This is highly common for small family-owned businesses.

Failure to Account for Output Tax on Deemed Supplies or Adjustments

Businesses often focus on sales, but certain non-sales transactions or changes in circumstances can trigger output tax liabilities.

The Mistake:

Business assets put to private use: If a business asset on which input tax was previously claimed is subsequently used for personal purposes, or given away without charge, output tax may need to be accounted for on its open market value.

Suppose a business disposes of an asset for no consideration or at a value significantly below its market value, and input tax was claimed on its purchase. In that case, output tax needs to be accounted for. This is a tricky situation as businesses often fail to account for GST during disposal.

Bad debt relief not reversed if recovered: If a GST-registered business claimed bad debt relief (reducing output tax) and subsequently recovers the debt, the original GST relief must be reversed.

Incorrect Application of Zero-Rating

While beneficial for export businesses, applying zero-rating incorrectly can lead to under-declaration of output tax.

The Mistake:

Zero-rating local supplies: Applying 0% GST to supplies that are consumed in Singapore. For example, charging 0% GST to a local customer for goods intended for export, but without sufficient evidence of export.

Insufficient evidence of export: For zero-rating to apply to exports of goods, businesses must retain official evidence of export (e.g., export permits, shipping documents, bill of lading). Without proper documentation, IRAS may deem the supply standard-rated, requiring the business to account for 9% GST.

Not all services provided to overseas customers can be zero-rated. The "International Services" provisions are complex and require the service to directly benefit an overseas person who is outside Singapore at the time the service is performed. Based on our experience, this is especially complex for services, rather than the provision of goods, as the beneficiary of services rendered may well be global or multi-geographical.

Poor Record-Keeping and Untimely Filing

While seemingly basic, lapses in record-keeping and late filing are common causes of penalties.

The Mistake:

Missing or incomplete records: Not retaining complete tax invoices, credit notes, debit notes, or other relevant documents for the required five-year period.

Inaccurate records: Errors in recording sales, purchases, input tax, or output tax amounts.

Late filing of GST returns: Failing to submit the GST F5 return by the due date (typically one month after the end of the accounting period).

Late payment of GST due: Failing to pay the net GST payable by the due date.

How to avoid the pitfalls and Errors of GST Filing

Most of the issues leading to errors in GST filing can be avoided with good foresight and planning. A visionary business leader or top management tends to balance growth and compliance in tandem. Let us explore some of the ways to ensure GST Compliance.

Systems and Internal Control: For companies, having the right system and internal control in place may be the first line of defense in ensuring GST Compliance. From working papers to IT infrastructure review and approval, having the correct procedures and workflow is essential for GST compliance. This could mean having the proper procedures for documenting GST records and having internal policies that serve as guidance on filing the right claims.

Data integrity: GST compliance, or Tax compliance in general, sits on the foundation of accurate and worthy data sets. Ensure your finance department or accounting team has the right capabilities, both experience and tools, to deliver a precise set of financial data within the filing deadline. Considering that GST filing is done 1 month after the quarter end, the bare minimum would be for your accounting team or accounting service provider to prepare quarterly accounts. While quarterly accounting may suffice, most would opt to prepare accounts every month as this gives greater clarity in performance tracking.

Digitalized: Closely related to Data integrity, digitalization is essential for record tracking, documentation, and accuracy. It is common for corporate service providers to use reputable accounting software such as Xero and QuickBooks to assist with accounting and taxation computation. Small businesses may still be reliant on Excel, but the competitive pricing for outsourced accounting may drive more business owners to digitalize and adopt software. In conjunction with most government agencies, digitalisation for tax compliance has been in development for many years. From the launch of myTax portal to having a digital self-help service, IRAS has been proactive in creating a seamless digitalised platform for compliance.

Reconciliation and Review: Reconciling your GST forms and workings is an essential step as part of your internal review. While big companies have strict and mature procedures in ensuring such checks and reviews are in place, smaller firms should proactively seek to incorporate such good practices.

Empowering employees: Having the right employees with the appropriate technical abilities will further reduce the occurrence of errors. Companies need to note that the capabilities of employees are closely tied to training and development. With evolving challenges and changing regulations, business management should always have a robust training policy to ensure that your people are adequately equipped with the correct skill set.

Partnering with a Professional Firm: GST Compliance and errors can be avoided most of the time when a company partners with a professional firm. Tax consultants from corporate service providers are usually experienced professionals who can assist companies in navigating the challenges of GST compliance and Tax issues. Priced competitively, consultants from a professional firm may also help you in implementing the proper tax controls or offer professional advice to improve tax compliance.

A special point to note: Errors relating to Employees’ Expense Claim

Employee expenses, while essential for business operations, often present unique challenges for GST claims due to their personal consumption element.

General Rule: GST can generally be claimed on employee expenses if they are incurred wholly and exclusively for the purpose of the business of the GST registered company, and are not for the private benefit of the employee or disallowed purposes (e.g., passenger cars).

Common Issues & Solutions:

Entertainment Expenses: While some entertainment expenses may be deductible for income tax purposes, the input tax incurred on most entertainment expenses (e.g., lavish dinners for clients, staff recreation) is generally not claimable unless the entertainment is provided for the purpose of making taxable supplies and is not primarily for the private enjoyment of the recipients.

Solution: Be clear on what constitutes business entertainment versus personal entertainment. Keep detailed records of the purpose of entertainment.

Overseas Travel Expenses: GST incurred on overseas travel (e.g., airfare, overseas accommodation) typically cannot be claimed as GST is a consumption tax levied in Singapore. However, GST on local components of overseas travel (e.g., local taxi fares to the airport, local hotel stays before an overseas trip) may be claimable if for business purposes.

Solution: Distinguish between local and overseas expenses. Only claim GST on Singapore-incurred expenses that meet input tax conditions.

Staff Welfare Expenses: GST on staff welfare expenses (e.g., annual dinner and dance, team-building events, pantry supplies) can generally be claimed if the costs are incurred for the benefit of all employees and are not excessive, and meet the "wholly and exclusively" for business purpose test.

Solution: Ensure such expenses are genuinely for staff welfare and not for personal gain.

Reimbursements vs. Direct Payments: When employees pay for business expenses and are reimbursed, the company can claim the input tax if the original tax invoice is addressed to the company, or if the employee provides a valid tax invoice and the company has a clear policy for claiming such input tax on reimbursements. If the company pays directly, the invoice must be addressed to the company.

Solution: Establish a robust expense claim policy requiring proper tax invoices and clear documentation for all business-related employee expenses.

Navigating these complexities requires vigilance and a solid understanding of GST principles. Many businesses find that engaging a specialized firm for Quarterly Accounting and GST advisory services is a cost-effective way to mitigate risks and ensure compliance.

GST Compliance: Importance and Penalties

For any GST registered company in Singapore, compliance is not merely an obligation; it's a critical aspect of responsible business operation that directly impacts financial stability and reputation. The Inland Revenue Authority of Singapore (IRAS) is vigilant in ensuring adherence to GST regulations, and non-compliance carries significant consequences.

Importance of Maintaining Compliance to Avoid Penalties

Maintaining robust GST compliance is paramount for several reasons:

Avoidance of Penalties and Fines: This is the most immediate and tangible benefit. IRAS imposes penalties for a wide range of non-compliant behaviors, including late filing, late payment, incorrect returns, and tax evasion. These penalties can range from financial fines to, in severe cases, imprisonment for individuals.

Reputation and Trust: A history of non-compliance can severely damage business reputation, not only with the authorities but also with customers, suppliers, and potential investors. A clean compliance record signals a responsible and trustworthy business.

Reduced Risk of Audits and Investigations: While IRAS conducts regular audits, businesses with a consistent record of timely and accurate GST filings are less likely to be subjected to intense scrutiny. Frequent errors or late submissions can trigger flags, leading to more thorough investigations that consume significant time and resources.

Optimized Cash Flow: Accurate and timely GST reporting ensures that businesses pay the correct amount of tax and receive legitimate refunds promptly. Errors can lead to overpayments, delayed refunds, or unexpected tax bills, all of which negatively impact cash flow. Having a good GST regime is part of efficient financial management.

Business Continuity: Severe non-compliance can lead to legal action, freezing of bank accounts, or even business closure in extreme scenarios. Adhering to GST rules safeguards the continuity of your operations.

Clarity and Control: Proper GST compliance necessitates meticulous record-keeping and transparent financial processes. This, in turn, provides business owners with a clearer and more accurate picture of their financial health, aiding better decision-making.

To truly grasp the gravity of non-compliance, consider this:

“In FY2023/2024, 2,521 GST audits were completed across various industries, resulting in a recovery of $162 million, including penalties.”

This staggering figure underscores IRAS's commitment to ensuring tax compliance and highlights the substantial financial repercussions for businesses that fail to meet their obligations. These amounts are not just taxes recovered but also include the additional financial burden imposed on businesses due to their non-compliance. A single significant error or prolonged period of non-compliance can lead to penalties that erode profits, strain cash reserves, and divert critical resources from growth initiatives to remedial actions.

Types of Penalties:

Late Filing Penalty: A flat penalty of S$200 for each month or part of a month that the return is late, up to a maximum of S$10,000.

Late Payment Penalty: Generally, a 5% penalty on the unpaid tax, with an additional 1% penalty for each completed month that the tax remains unpaid, up to a maximum of 15% of the tax due.

Penalties for Incorrect Returns: This can range from a 100% to 200% penalty on the undercharged tax, depending on whether the error was due to carelessness or willful intent to evade tax. In some cases, fines and imprisonment may also be imposed.

Failure to Register for GST: If a business fails to register for GST when it is legally required to do so, IRAS can impose a penalty of up to 10% of the tax due from the date it should have registered, plus an additional penalty of up to 200% of the tax undercharged.

Given the potential financial and reputational damage, the cost of proactive compliance pales in comparison to the risks associated with non-compliance. It is an investment in your business's stability and future.

The Role of Corporate Service Providers: Your Partner in GST Management

In the dynamic and often intricate landscape of Singapore's business environment, particularly concerning tax compliance like GST, the strategic advantage of engaging professional corporate service providers cannot be overstated. While it's tempting for new businesses or those focused on cost-cutting to manage everything in-house, the complexities of GST regulations, coupled with the potential for severe penalties from non-compliance, make a tax agent's assistance a wise investment. For any GST registered company in Singapore, a reliable corporate service provider becomes an indispensable partner, ensuring accuracy, efficiency, and peace of mind.

Imagine a business journey where you can dedicate 100% of your focus to innovation, market expansion, and customer satisfaction, knowing that the intricate web of tax compliance is expertly managed.

This is not a distant dream but a tangible reality when you partner with a seasoned corporate service provider. In Singapore's competitive ecosystem, time is your most valuable asset. Every hour spent grappling with tax forms, deciphering complex regulations, or correcting accounting errors is an hour diverted from revenue-generating activities and strategic growth.

A corporate service provider isn't just an expense; they are an extension of your team, a specialized unit bringing deep expertise in Singaporean tax laws and best practices. They don't just fill out forms; they strategically advise, identify potential risks, and optimize your GST position to ensure maximum legitimate input tax claims and minimal liabilities.

Consider having a professional tax service provider akin to a compliance officer-cum-insurance. They help you navigate regulations and serve as a safeguard against costly mistakes for your business.

A good corporate service provider may even take up the role of an advisor, offering recommendations and advice as your business grows.

Perhaps businesses should consider reclaiming precious time and focus on what truly drives their business forward, while leaving the complexities of GST to the experts?

Benefits of having a Tax Advisor or Tax Consultant

Engaging corporate service providers offers a multitude of benefits for businesses managing their GST obligations.

Expertise and Up-to-Date Knowledge

Benefit: Corporate service providers employ tax specialists who possess in-depth knowledge of Singapore's GST laws, including the latest amendments, schemes, and rulings by IRAS. They understand the nuances of various industries and how GST applies to specific business models. These tax experts are also proficient in cross-border payments and transactions, which may complicate matters.

Impact: This expertise minimizes the risk of errors, incorrect claims, or missed opportunities for tax savings. You benefit from proactive advice on complex transactions and changes in regulations, ensuring your business remains compliant and agile.

Ensured Compliance and Reduced Penalty Risk

Benefit: Professionals ensure that all GST filings are accurate, complete, and submitted on time. They meticulously prepare GST returns (Form 5), handle input tax claims, and ensure proper documentation is in place. Having a professional team can also be ideal for building up your existing members' capabilities, a practice many large companies often adopt. In a broader scheme, it serves as a cross-check, assuming one already has an in-house team.

Impact: This dramatically reduces your exposure to penalties for late filing, late payment, or incorrect declarations. It provides peace of mind, knowing that your compliance is handled by dedicated specialists, safeguarding your financial health and reputation.

Efficiency and Time Savings

Benefit: Outsourcing the filing of GST tax returns frees up your internal resources. Business owners and their teams can focus on core competencies, strategic initiatives, and revenue-generating activities instead of spending valuable time on administrative tax tasks.

Impact: Increased productivity and a more efficient allocation of internal talent lead to accelerated business growth and innovation.

Cost-Effectiveness

Benefit: While there is a fee for professional services, this cost is often outweighed by the benefits. Hiring and retaining an in-house GST expert can be more expensive, considering salary, benefits, training, and the cost of specialized software. Moreover, avoiding just one significant penalty can easily justify the cost of professional services.

Impact: You gain access to high-level expertise without the overheads of a full-time employee, transforming a potential fixed cost into a more flexible operational expense.

Robust Record-Keeping and Audit Preparedness

Benefit: Corporate service providers implement systematic and rigorous record-keeping practices. They advise on the necessary documentation for all transactions and ensure records are maintained in an organized and accessible manner for the statutory retention period.

Impact: In the event of an IRAS audit or review, your business will be well-prepared, with all necessary documentation readily available, streamlining the process and increasing the likelihood of a favorable outcome. Having proper documentation is the first line of defense.

Strategic Advisory and Tax Planning

Benefit: Beyond mere compliance, good corporate service providers offer strategic GST advisory. They can help you understand the GST implications of new business ventures, restructuring, or international expansion, providing insights that can optimize your tax position.

Impact: This proactive approach allows you to make informed business decisions, potentially unlocking tax efficiencies and ensuring that your growth strategies are tax-optimized from the outset.

Support for Specific Schemes:

Benefit: They can guide your business through applications for schemes like the Major Exporter Scheme (MES), Import GST Deferment Scheme (IGDS), or others that can significantly improve your cash flow by deferring or exempting GST payments at the point of import or purchase.

Impact: Leveraging such schemes effectively requires a detailed understanding and precise application, which corporate service providers can facilitate, leading to substantial financial advantages.

For businesses aiming for sustainable growth in Singapore, particularly those evolving into a fully GST registered company, partnering with a competent corporate service provider is not just a convenience—it's a strategic imperative. It's an investment in robust financial governance, risk mitigation, and ultimately, your company's long-term success.

Conclusion: Impact and Management of GST in Business

The Goods and Services Tax (GST) is an undeniable and integral component of Singapore's tax landscape, significantly impacting businesses of all sizes, from nascent startups undergoing Singapore business incorporation to established multinational corporations. As we've navigated through the various facets of GST – its fundamental principles, the strategic considerations of voluntary registration, the intricacies of import and export, and the pitfalls of non-compliance – a clear theme emerges: effective GST management is not just about adhering to rules; it's about strategic financial governance that can profoundly influence a business's operational efficiency, profitability, and reputation.

The impact of GST reverberates across almost every department and process within a GST registered company:

Financial Operations: GST directly affects cash flow. Businesses collect output tax from customers and pay input tax on purchases. The net amount impacts the funds available to the business. Accurate Quarterly Accounting is the bare minimum for an accounting department to support GST compliance.

Pricing Strategies: Companies must factor in GST when setting prices for their goods and services. For B2C businesses, this can influence consumer perception and competitiveness. For B2B transactions, while recoverable by the buying business, it still needs to be correctly charged and accounted for.

Administrative Burden: Compliance demands meticulous record-keeping, accurate invoice issuance, and timely submission of returns. This requires dedicated resources, whether human capital or technological solutions.

Supply Chain and International Trade: For businesses involved in imports and exports, GST considerations are complex, requiring an understanding of zero-rating rules, import GST deferment schemes, and customs procedures. Missteps here can lead to significant financial leakage or delays.

Risk, Compliance, and Reputation: Non-compliance carries severe penalties, including fines and reputational damage. A clean compliance record is a hallmark of a well-managed and responsible enterprise.

In light of this pervasive impact, the imperative for stringent GST compliance cannot be overstated. It is the cornerstone of sustainable business operations in Singapore. However, for many business owners, particularly those who are not tax specialists, managing these complexities can be a daunting and time-consuming endeavor. This is precisely where the invaluable role of professional corporate service providers comes into sharp focus.

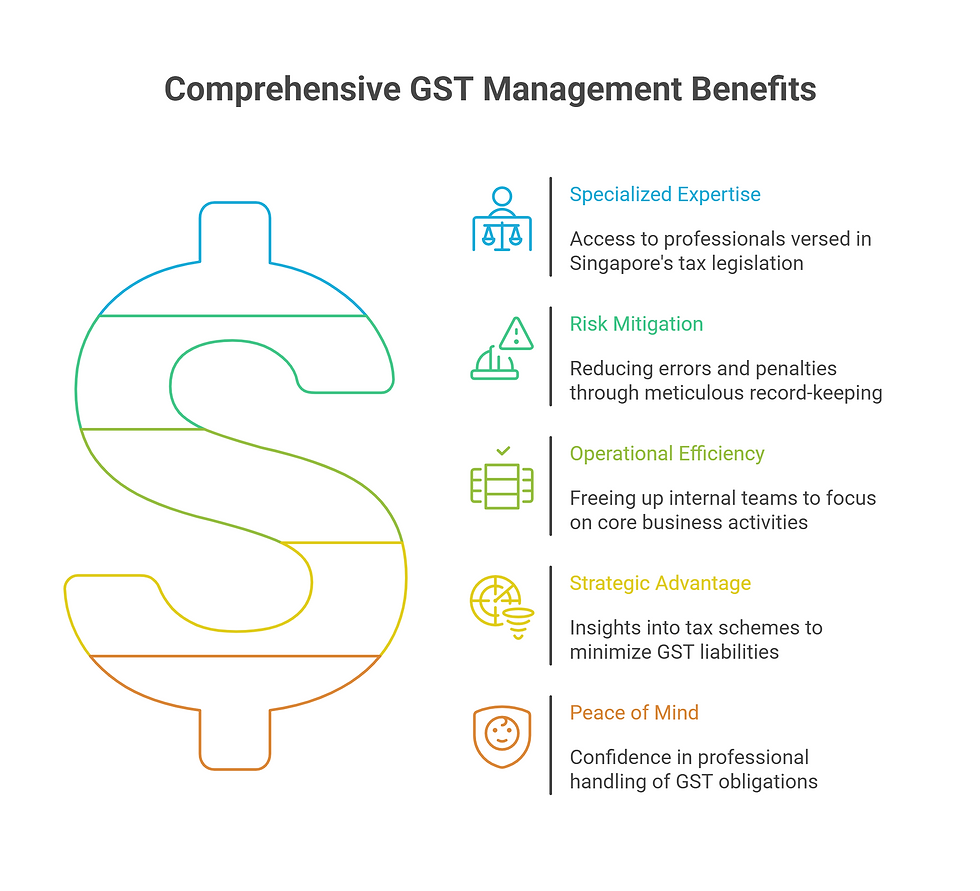

Engaging a reputable corporate service provider for your GST management offers:

Specialized Expertise: Access to professionals deeply versed in Singapore's tax legislation, ensuring that your business benefits from accurate advice and optimal GST planning.

Risk Mitigation: Significantly reducing the likelihood of errors, late filings, and non-compliance penalties through meticulous record-keeping and timely submissions.

Operational Efficiency: Freeing up your internal team to concentrate on core business activities and strategic growth, rather than getting bogged down in administrative tax tasks.

Strategic Advantage: Gaining insights into available tax schemes and opportunities to minimize your GST liabilities and improve cash flow legally.

Peace of Mind: Confidence that your GST obligations are being handled professionally and in accordance with IRAS requirements, allowing you to focus on your entrepreneurial vision.

In conclusion, GST in Singapore is more than just a tax; it's a critical element of your business's financial health and operational framework. By embracing a proactive approach to GST management, understanding its nuances, and crucially, leveraging the expertise of professional corporate service providers, businesses in Singapore can not only ensure compliance but also transform their GST obligations into an advantage for sustained growth and success in this vibrant global business hub.

Embrace innovative and professional GST management services, and unlock your business's full potential.

Get in touch with our team to find out how we can help.

DISCLAIMER: The views and opinions expressed in this article are those of the author and do not necessarily represent the views and opinions of any individuals or organizations with which the author may be affiliated, either in a professional or personal capacity, unless explicitly stated.

Comments